Signs of recovery European labelstock demand at the end of 2023

17 marzo 2024

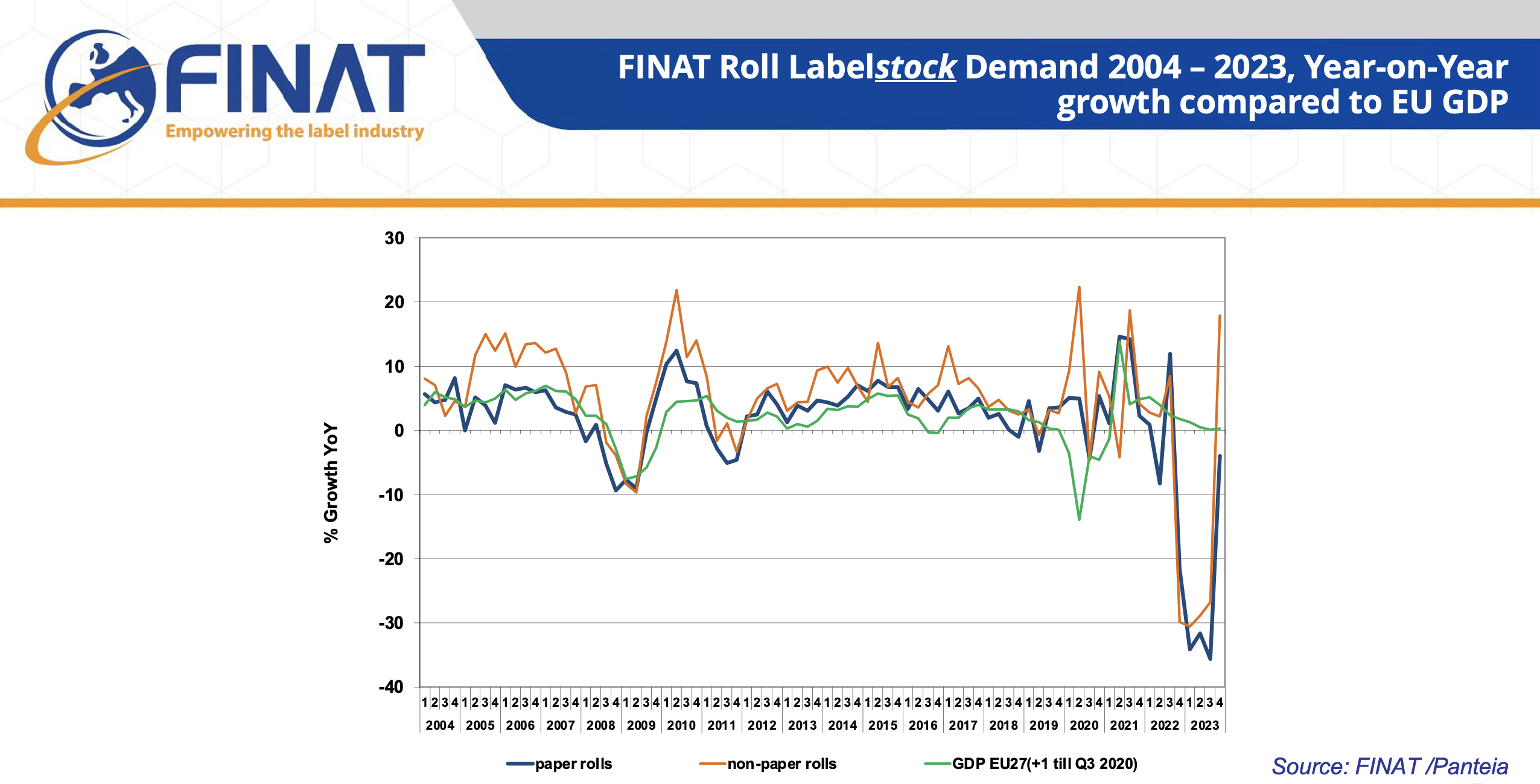

In the fourth quarter of 2023, labelstock demand in Europe increased by 2.1% compared to the same quarter in 2022. After first signs of a slowing of the decline emerged in the summer of 2023, the industry is set for continued recovery in 2024.

In the fourth quarter of 2023, labelstock demand in Europe increased by 2.1% compared to the same quarter in 2022. This was the first increase after four quarters of dramatic double-digit decline that started in Q4 2022, as the toxic mix of subsequent post-Covid excess demand, raw materials shortages, stockpiling, supply chain disruptions, cost increases and economic decline hit hard on the label industry throughout the year 2023. After first signs of a slowing of the decline emerged in the summer of 2023, the industry is set for continued recovery in 2024.

Compared to 2022, European consumption of self-adhesive label materials decreased by no less than 25.8%, the sharpest decline in a single year recorded since FINAT started the collection of statistics in 2003.

According to the latest FINAT Radar published in February, the pattern of decline in labelstock consumption was similar across major end-use segments including food, beverages, and health and beauty care, all sectors that showed promising signs of recovery in the final quarter of 2023.

European roll labelstock demand in m2, growth versus same quarter in previous year compared to GDP, 2004 - 2023

Stockpiling effect

The decline of European labelstock demand was more prominent and prolonged than outside Europe and compared to other sectors in the labelling and packaging domain. One important explanation is the excessive stockpiling effect that was triggered by the prolonged paper industry strike in Q1 2022, resulting in battle for raw materials (notably paper-based release liners and label facestock materials) and lead times of 3-5 months. When raw materials availability finally returned to normal in the third quarter of 2022, the economic tide had turned and label printers and label users had filled their warehouses for quarters to come. The downturn was compounded by the effect of increasing raw materials costs that, according to the FINAT RADAR, impacted the procurement of labels more than other packaging types.

Brand-owner challenges

According to the report, during the brand owner survey and in-depth interviews conducted for this edition, respondents highlighted the significant challenges they encountered due to evolving consumer demands. These challenges included a noticeable shift in consumer preference from branded products to private labels, alterations in seasonal demand patterns, and an oversupply of materials for certain stock-keeping units (SKUs) triggered by an abrupt drop in demand. These insights underscore the complex and dynamic nature of the market.

Brighter outlook

The decline in consumer confidence across the eurozone, as indicated by the European sentiment indicator, continues to reflect widespread concerns about inflation, energy costs, and the potential for economic downturn. However, the slightly brighter outlook from label suppliers and brand owners suggests optimism about the capacity for recovery and growth in the coming quarters.

Sfoglia le Riviste

Follow us

© Copyright 2026. PrintPUB.net - N.ro Iscrizione ROC 35480 - Privacy policy