The printing industry, signs of optimism

8 maggio 2024

The 9th drupa Global Trends Report revealed that confidence levels were found to be growing across all markets and almost all regions, despite challenging economic headwinds.

The first drupa Global Trends Report since the Covid pandemic was remarkably positive as the ever-resilient print industry bounced back, reporting a more positive condition than in 2019 i.e. before COVID19. The results this year have maintained that momentum, with a further improvement in sentiment for 2023 and very positive expectations for 2024.

Economic confidence by regions and markets

Globally in 2023, 44% stated their company’s current economic situation was ‘good’, and 12% described it as ‘poor’ while the remaining 44% described it as ‘satisfactory’. The net positive balance being +32% i.e. 44% minus 12%, is the overall result shown as the green column in the chart, 14% better than in 2022. It is this net positive or negative balance that is shown in many of the charts that follow. It is not all good news. Germany was downbeat at +12%, the same as 2022. Yet the Rest of Europe was +34%. North American (N. America) sentiment softened to +50% from the peak last year. However, South/Central America (S/C. America) +24%, Africa +34%, Middle East +52% (small data set) and Australia/Oceania +56% (small data set) all recovered well from previous lows. Looking ahead, all regions, except Australia/Oceania, expect better performance in 2024, although Germany at just +4% is far more cautious than most.

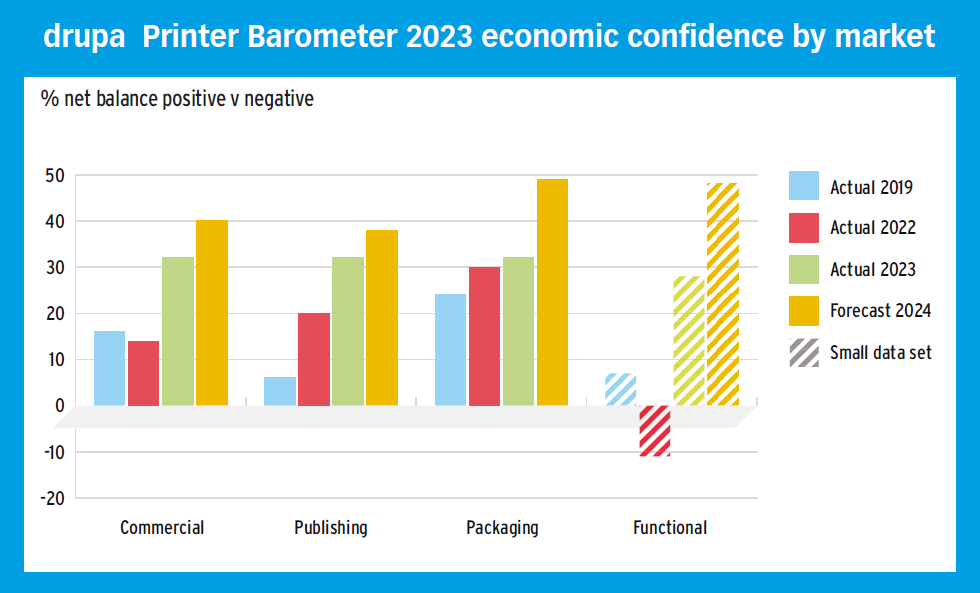

Looking at markets, there is a striking recovery in confidence amongst Commercial and Publishing printers across the globe, while Packaging continues in its confident fashion. The unexplained dip in confidence for Functional print in 2022 is reversed – probably a result of the small data set.

Suppliers were a little more cautious this year than last at 32%, down 2%. N. America, S/C. America and Asia were up, with Europe down 5%. All markets were fairly flat this year, but all showed great confidence for next year, perhaps in part because of drupa 2024! For the second year running, printers raised prices globally; this after seven years of falling prices.

Revenues grew at the fastest rate by far and margins decreased at the slowest rate ever recorded. The pattern was not universal, with Europe and S/C. America reporting a more mixed situation. Suppliers reported a similar upbeat assessment.

Commercial pricing is strong, net balance average +57% for the last two years compared with an average of -21% 2013-2017. Publishing is also an average +57% last two years; average -18% 2013-2017.These figures suggest the beginnings of better times for both market sectors. The stronger financial performance for the industry as a whole is welcome, as long as it does not crumble under wider inflationary pressures.

Changes in print volume by technology

Every year we ask printers to assess the net print volume by print technology. The resilience of sheetfed offset is remarkable with net growth in all markets, even commercial after a number of years of reductions. Flexo grows fast in packaging and Digital toner cutsheet colour is far ahead of all other digital processes in all markets.

Globally the digital adoption rate – printers claiming more than 25% of turnover in digital – is growing from 26% in 2014 to 29% in 2023. At first sight this is only a modest growth. However, according to various industry sources volumes have grown significantly since 2014, even though the digital adoption rate appears to be slowing down. 25% of the total printer panel reported having web-to-print installations in 2014. The figure for 2023 is still 25%. Some regions have less e-commerce for cultural, technical and other reasons but the figure is flat almost everywhere.

Those operating web-to-print enjoyed a surge in demand from that source over the Covid period, but demand has fallen back this year almost to pre-Covid levels. The exception is Packaging where the major growth of 2022 has been largely maintained.

Labour shortages are reported by both printers 47% and suppliers 39%. Conventional press operators and finishing staff are hardest to recruit for printers and manufacturing and technical support staff amongst suppliers. Supply chain issues have loomed large for both Printers 63% and Suppliers 73%, although all expect issues to be less next year.

Global capital investment

Capital expenditure fell back during the pandemic and there was an inevitable lag in 2022 but demand picked up strongly in 2023 with even higher forecasts for 2024. There was the expected sustained demand from Packaging printers, and an encouraging surge from Commercial and Publishing printers, while Functional printers retuned to levels not seen since 2018. As usual, print technology and finishing equipment are the strongest targets by far.

Sheetfed offset remains first choice for print technology globally and has been since the first Trends report in 2014. Digital presses take the next two places for popularity. There is more variety when analysing the market sectors, signalling the amazing range of products and market conditions that together dictate best investment choices.

Capital expenditure amongst suppliers was relatively flat at just +4% net balance. However, all were bullish for 2024 at +24% across all markets, particularly for the Functional market. Building sales channels, raising efficiencies and developing new services are the preferred targets.

Both printers and suppliers have increasingly relied on diversification to create growth, though the rate of change is slower as trading has returned to more normal patterns post-Covid.

Socio-economic issues loom as large as ever over all regions. The risk of economic recession is the top concern 47%, knocking the impact of pandemics into second place 41%.

However, beyond the top two issues there were major variations across almost every region. For example, S/C. American printers were concerned about Political instability 52%, African printers highlighted currency issues 51%, Australian printers pointed to environmental issues 33%, Asian printers commented on trade wars 23% and N. American printers worried about standards of living 32%. Opinion is divided between those that think market forces are more important 43% and those who think socio-economic forces 46%.

We returned to market specific questions for the first time since 2019. For commercial markets, the key takeaway is the advantages of diversification in both markets served and services offered.

The proportion of publishing printers in the sample has halved since 2014 (from 30% of the total 2014 to 15% in 2023).

And the mix of markets they serve has also changed, with fewer in the newspaper, magazine and catalogue markets but more offering varying book printing options. Packaging printers report increasing demand for added value packaging e.g. interactive print. The search for more environmental alternatives to plastic packaging is a major focus for many, particularly for Flexible printers of course. While our sample of Functional printers is small, the shift to inkjet print from screen and toner is clear.

In conclusion

The majority of printers and suppliers across the globe have increasing confidence for the future, despite the many market and socio-economic risks and challenges. Prices and revenues are up strongly and the squeeze on margins is less than ever. The question is whether the industry will remain as positive in the face of inflationary pressures.

Perhaps the most encouraging news is the clear improvement in confidence amongst Commercial and Publishing printers, who appear to have adapted to the impact of the digital revolution and can plan forward with greater confidence. Meanwhile Packaging printers enjoy sustained demand and Functional printers continue to enjoy an astonishing and ever-growing variety of products and markets served. Capital expenditure has recovered to pre-Covid levels and 2024 is forecast to be a bumper year for investment – good for drupa 2024!

Source: drupa Global Trends Report

Sfoglia le Riviste

Follow us

© Copyright 2024. PrintPUB.net - N.ro Iscrizione ROC 35480 - Privacy policy